2025 Q3 Global Shipping Market Outlook

The current global economy and geopolitical landscape are affected by multiple uncertainties. Tensions between Israel and Iran, especially issues surrounding the Strait of Hormuz, are threatening regional stability and energy supply routes. Houthi activities in the Red Sea also pose risks to Suez Canal shipping. Ongoing oil sanctions continue to disrupt the global energy market, while adjustments in U.S. import tariffs further complicate international trade dynamics. Additionally, uncertainty in China’s GDP growth casts a shadow over the strength of global economic recovery.

Below is Veson Nautical’s market forecast and analysis for the tanker, bulk carrier, container ship, and gas carrier sectors, based on platform data, under these uncertain factors for Q3 2025.

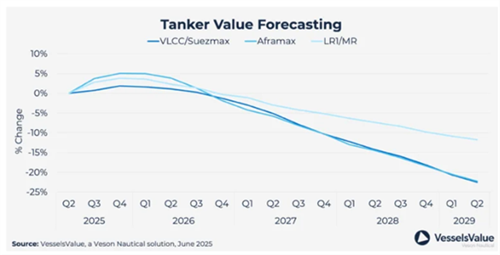

Tankers

Geopolitical risks, sanctions, and shifts in trade flows—mainly driven by Red Sea tensions and the EU ban on Russian oil—continue to drive tanker freight rate volatility and stimulate growth in ton-mile demand.

Long-haul rerouting of crude trade from the Atlantic to Asia supports vessel utilization, but new vessel deliveries, improved fuel efficiency, and the global shift to decarbonize oil demand exert downward pressure.

As demolition rates remain low and new orders and deliveries rise, fleet growth is expected to outpace demand after 2025. However, regulatory pressures from the EU Emissions Trading System (EU ETS) and IMO decarbonization targets may partially offset this trend.

Electrification of energy, improved engine efficiency, and shifts in consumption behavior are structurally suppressing oil demand, signaling long-term challenges for tanker trade volumes.

China remains a key variable for oil demand and trade volumes, but overall weak Asian demand, macroeconomic vulnerabilities, and inflationary pressures are reshaping global consumption patterns.

Although the Red Sea crisis in 2024 spurred a surge in container ship and tanker orders, new vessel orders in 2025 have fallen sharply. Newbuild prices remain high, but may gradually decline as shipyard capacity pressures ease.

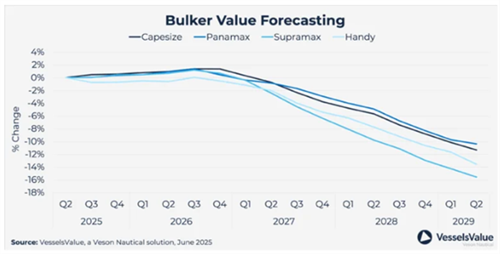

Bulk Carriers

New vessel ordering has slowed in recent years, with bulk carrier orders at low levels. Slower supply growth is pushing the market towards a supply-demand balance, but tariff policies and trade disruptions continue to create demand uncertainty.

Challenges to China’s economic growth, especially a sluggish real estate sector and over-reliance on exports, are expected to weaken dry bulk import demand in 2025, negatively impacting market balance.

In the long term, ton-mile demand is expected to grow, primarily driven by new trade routes such as Guinea–China iron ore shipments following the start-up of Simandou in 2026.

Persisting geopolitical tensions—particularly potential renewed Houthi attacks in the Red Sea—could maintain vessel rerouting, potentially adding about 1% to ton-mile demand and supporting freight rates.

Stimulated by Red Sea rerouting and freight rate recovery in 2024, container ship orders surged to record highs, boosting shipyard capacity utilization. However, order activity has significantly slowed in the first half of 2025.

Currently, the newbuilding-to-existing fleet ratio for container ships and LNG carriers remains high. Persistently high newbuild prices are expected to curb future order growth, easing shipyard capacity pressure and potentially leading to a gradual decline in newbuild prices.

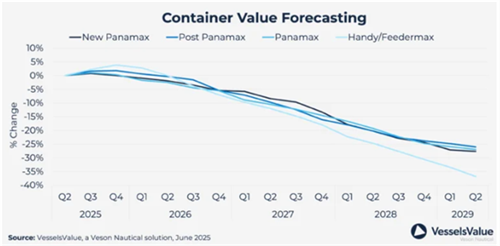

Container Ships

Freight rates remained firm from 2024 to early 2025, but as fleet growth outpaces demand, rates are expected to steadily decrease from mid-2025, with idle vessel numbers likely to rise.

The surge in new orders in recent years has driven rapid fleet expansion: net growth was 5.5% in 2023, 9.7% in 2024, and is projected to average 8.2% per year from 2025 to 2028.

In 2024, container ship orders hit a record 4.3 million TEU, with the orderbook-to-fleet ratio rising to 31.1%. Route adjustments are shifting market preference from New Panamax vessels to ultra-large container vessels (ULCVs).

Ship demolition has been limited, but is expected to moderately increase, especially for vessels under 3,000 TEU, as operating older ships becomes less economical amid falling freight rates.

Following two order booms during the pandemic and the 2024 Red Sea crisis, container ship ordering activity has cooled significantly in 2025. High order volumes and persistently rising newbuild prices are expected to suppress future ordering and ease shipyard capacity pressure.

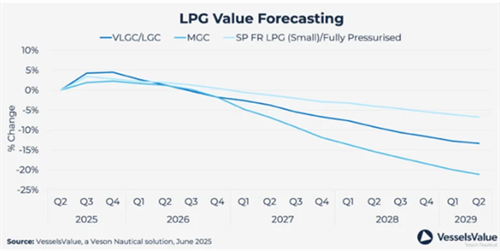

Gas Carriers

U.S. LPG production grew 5.9% in 2024, but is expected to slow to 4.2% in 2025. Export growth will also ease due to terminal capacity constraints, but is expected to rebound from 2026 as new facilities come online.

The VLGC/VLAC fleet expanded by 10.9% in 2024, with an average annual growth rate of 7.3% expected through 2028. Despite robust demand, the recent surge in new orders may pressure earnings, while the fleet remains young and demolition rates are low.

The mid-size LPG vessel fleet is seeing strong growth (about 10.8% per year), while the small vessel segment faces a lack of new orders and an aging fleet, leading to persistently high scrapping rates.

VLGC daily earnings held at $43,300 in 2024, but are expected to decline in 2025 as U.S. export growth slows. Earnings may briefly rebound in 2026 with terminal expansions, but oversupply will likely cause another drop in 2027-28. Panama Canal conditions remain stable but are still affected by seasonal water level fluctuations.

Amid trade uncertainties—especially in U.S.-China trade—the petrochemical and natural gas industries face overcapacity and weak demand. However, increased intra-Asia trade activity and macroeconomic improvements may support a mid-term recovery in cargo volumes.

Source: Veson Nautical